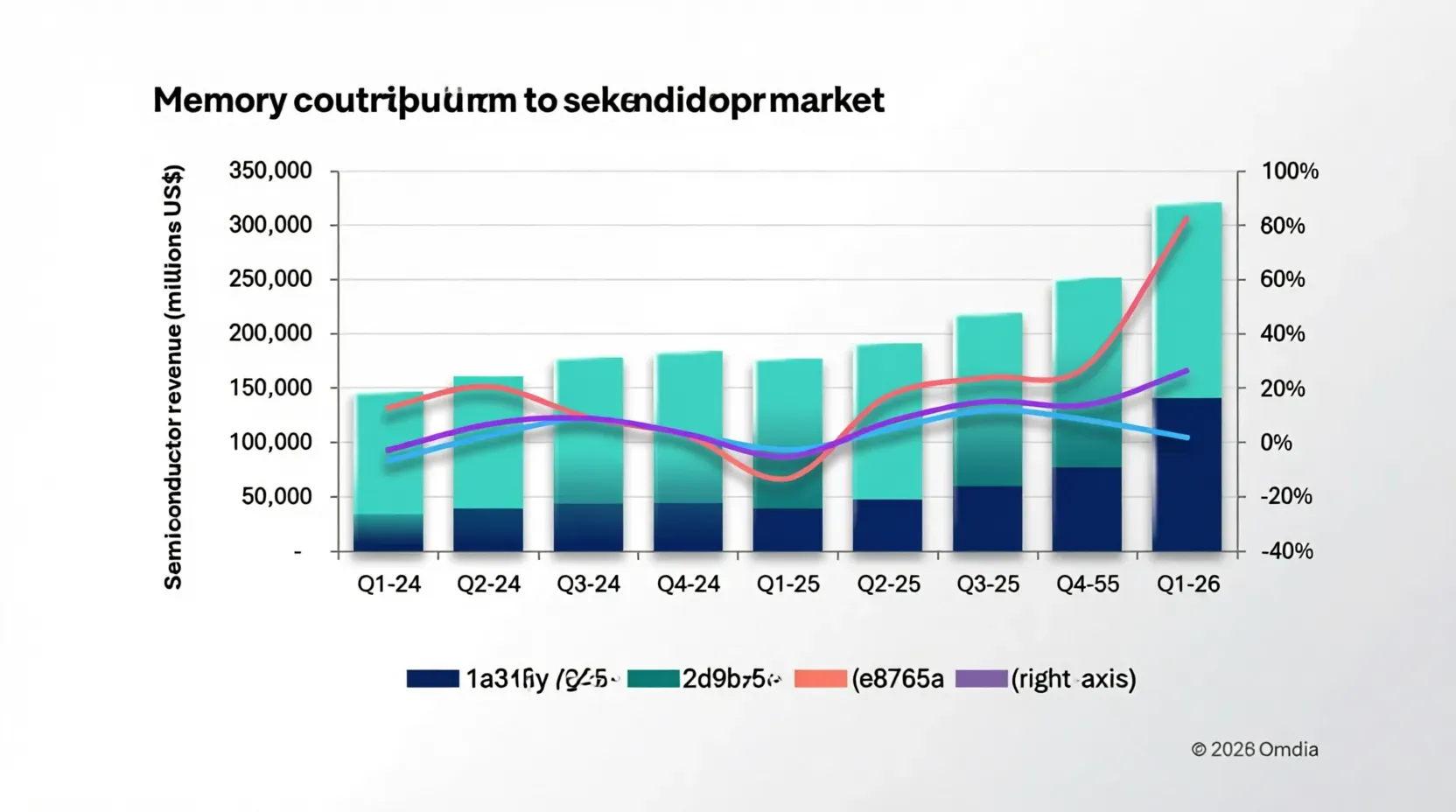

The semiconductor industry entered 2026 on a historic upswing, with total market revenue climbing to $319 billion in the first quarter—a 27 % jump from the previous quarter. This surge marks the strongest quarter‑over‑quarter growth recorded since Omdia began its quarterly tracking in Q1 2002. The primary catalyst was an unprecedented rise in memory‑chip sales, especially dynamic random‑access memory (DRAM) and NAND flash, whose revenues almost doubled in just three months. Analysts attribute this acceleration to a confluence of factors: relentless AI‑driven compute demand, tight supply conditions caused by technology transitions, and a product‑mix shift that lifted average selling prices (ASPs). For enterprise data‑center operators, the rapid expansion of memory revenue signals potential capacity‑planning challenges and pricing pressure that could shape procurement strategies throughout the year.

Omdia Reports Record Quarterly Revenue for the Semiconductor Industry

Omdia’s latest quarterly market tracker confirms that semiconductor revenue grew 27 % from Q4 2025 to $319 bn in Q1 2026, delivering the steepest QoQ increase in the dataset that spans back to Q1 2002. Memory revenue alone surged over 80 % sequentially, propelling the overall market toward a projected $700 bn total for the first half of 2026. The report highlights three consecutive quarters of double‑digit growth, and Omdia expects the pattern to persist into Q2 2026, albeit at a slightly slower pace. The firm also notes that AI‑related demand remains a key engine, while ongoing memory supply‑demand imbalances continue to dominate market narratives.

Memory Chips Account for Over 40 % of Q1 2026 Semiconductor Sales

DRAM and NAND flash together accounted for more than 40 % of total semiconductor revenue in Q1 2026, a stark contrast to the long‑term average of roughly 20 %. Within this segment, NAND flash emerged as the standout performer: revenue reached just under $48 bn, up 96 % QoQ, while NAND ASPs climbed 95 % sequentially. Omdia links this price escalation to sustained AI and data‑center demand, coupled with supply constraints tied to technology transitions, yield learning curves, and product‑mix challenges. Utilization rates remain high, and the limited pace of supply recovery reinforces the upward pressure on both revenue and pricing. The firm anticipates that this momentum will extend into Q2 2026, supporting continued growth for memory components.

Non‑Memory Semiconductor Segments Show Modest Growth

When memory revenue is stripped out, the remainder of the semiconductor market posted a modest just‑over‑2 % QoQ increase in Q1 2026. Historically, both overall and non‑memory semiconductor revenue tend to decline by about 4 % in the first quarter, making this modest rise noteworthy. Microcontrollers (MCUs), discretes, and optical components experienced slight to mid‑single‑digit declines, reflecting typical seasonal patterns. In contrast, components tied to AI and data‑center workloads outperformed the seasonal dip, providing a buffer that lifted the non‑memory segment into modest growth territory. This divergence underscores how AI‑centric demand is reshaping performance across traditionally stable semiconductor categories.

Outlook for the Rest of 2026

Omdia projects that Q2 2026 will continue to deliver strong growth, though at a slower rate than the 27 % surge seen in Q1. Sequential growth for the overall semiconductor market is expected to exceed 20 %, keeping the first‑half‑2026 total on track to surpass $700 bn. Clifford Leimbach, Practice Leader at Omdia, emphasized, “Four consecutive quarters of double‑digit revenue growth for the market show the strength of the current demand for semiconductors.” He added that this trajectory could push total 2026 revenue beyond the $1 tn threshold.

Key Takeaways

- Semiconductor revenue reached $319 bn in Q1 2026, a 27 % increase from Q4 2025, the highest QoQ growth recorded since Omdia began tracking the market in 2002.

- Memory chips (DRAM and NAND) contributed over 40 % of total semiconductor revenue, with NAND revenue rising 96 % QoQ to just under $48 bn and ASPs climbing 95 % sequentially.

- Excluding memory, non‑memory semiconductor revenue grew just over 2 % QoQ, contrasting with the typical 4 % seasonal decline for this segment.

TechInsyte's Take

The pronounced memory‑driven growth suggests that enterprise data‑center planners may face tighter supply and higher pricing for DRAM and NAND in the near term. While non‑memory segments remain relatively stable, the overall market’s double‑digit momentum signals continued capital‑expenditure pressure on AI‑related workloads. Buyers should monitor supply‑chain constraints and price trends through Q2 2026 to inform procurement and capacity‑allocation decisions.

Source: Businesswire