Snowflake (NYSE: SNOW) reported its first‑quarter fiscal 2027 results, ending April 30, 2026, highlighting a 34% year‑over‑year increase in product revenue to $1.33 billion. The company cited accelerating AI adoption, new enterprise customers, and expanded partnerships as drivers of the “strongest sequential dollar growth in our history.”

Snowflake Announces Q1 FY27 Financial Highlights

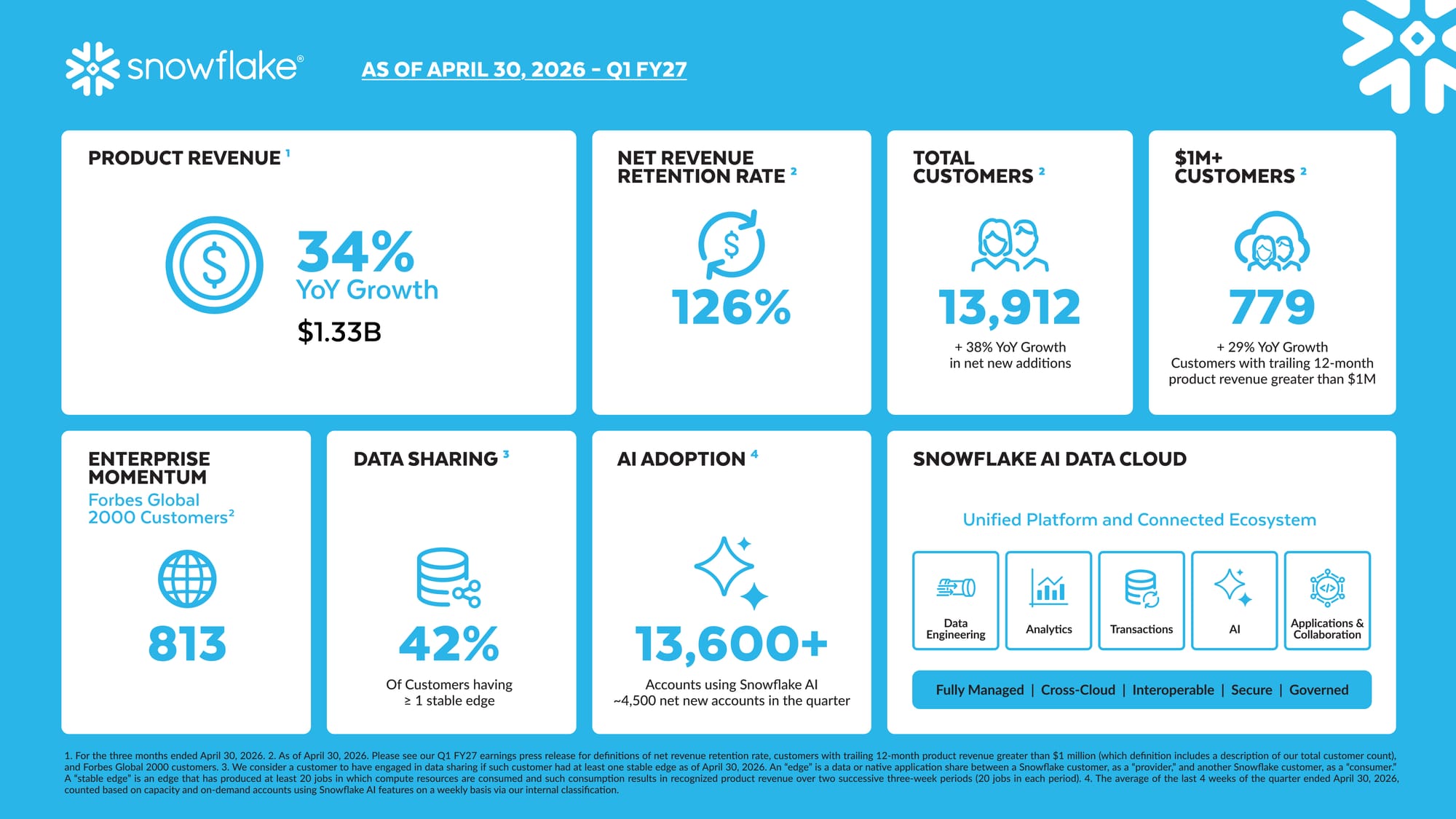

Snowflake delivered $1.33 billion in product revenue, up 34% YoY, and total revenue of $1.39 billion, up 33% YoY. Net revenue retention reached 126%, and the firm counted 779 customers with trailing 12‑month product revenue exceeding $1 million—a 29% YoY increase. The customer base now includes 813 Forbes Global 2000 firms, and remaining performance obligations grew 38% YoY to $9.21 billion.

AI‑Centric Product Expansion and Partnerships

The quarter saw more than 13,600 accounts using Snowflake AI capabilities, with Snowflake Intelligence usage more than doubling QoQ and Cortex Code deployed across over 7,100 accounts. New customers such as Holiday Inn Club Vacations and Houzz adopted Snowflake as the core of their data and AI initiatives. Snowflake also announced a $6 billion multi‑year agreement with AWS to accelerate enterprise AI adoption, deepened its partnership with OpenAI, and made its SAP‑derived capabilities generally available. In May 2026, Snowflake signed a definitive agreement to acquire Natoma, a Model Context Protocol platform for AI agents, to extend governance to AI‑driven workflows.

Outlook and Guidance for FY27

For Q2 FY27, Snowflake projects product revenue of $1,415 million–$1,420 million (30% YoY growth) and a non‑GAAP operating margin of 12.5%. Full‑year FY27 guidance now targets $5,840 million in product revenue (31% YoY growth), up from the prior $5,660 million outlook, and a non‑GAAP operating margin of 13.5%. The company also expects a non‑GAAP product gross margin of 75.0% and an adjusted free‑cash‑flow margin of 23.0%.

Key Takeaways

- Product revenue reached $1.33 billion in Q1 FY27, a 34% YoY increase and the strongest sequential dollar growth in Snowflake’s history.

- AI‑related usage grew sharply: accounts using Snowflake Intelligence more than doubled QoQ, and Cortex Code is active in over 7,100 accounts.

- Snowflake raised full‑year product‑revenue guidance to $5.84 billion, reflecting 31% YoY growth expectations.

TechInsyte's Take

Snowflake’s Q1 results underscore the momentum of its AI‑enabled data platform and the impact of strategic cloud partnerships. While the raised guidance signals confidence, the company’s reliance on consumption‑based revenue and ongoing AI rollout introduces execution risk. CIOs and data leaders should monitor adoption rates of Snowflake Intelligence and Cortex Code, as well as the integration outcomes of the Natoma acquisition, to gauge the platform’s suitability for enterprise AI workloads.

Source: Businesswire